Ask any bookkeeper or accountant what the single most important habit in their job is, and there’s a good chance they’ll say the same thing: get your journal entry right, and everything downstream falls into place. Get it wrong, and you’ll spend hours later untangling a mess.

I’ve seen this play out firsthand. A small business owner once told me she’d been “balancing” her books for months, only to discover a single misclassified entry had thrown off her entire quarterly report. That’s the thing about a journal entry, it seems small on the surface, but it carries a lot of weight.

In this guide, we’ll break down exactly what a journal entry is, why it matters so much, and how you can record entries accurately without the headaches. Whether you’re a student learning the basics or a small business owner managing your own books, this one’s for you.

What Is a Journal Entry, Exactly?

At its core, a journal entry is simply a record of a financial transaction in a company’s accounting system. Every entry follows the double-entry system, meaning it always includes at least one debit and one credit, and the two must balance.

Here’s a simple way to think about it: every time money or value moves in your business, something needs to be written down. That “something” is the journal entry.

A basic journal entry typically includes:

- The date of the transaction

- The accounts affected (debit and credit)

- The amount involved

- A brief description or memo

Quick takeaway: If you remember nothing else, remember this — every journal entry must balance. Debits always equal credits.

Why Journal Entries Matter More Than People Think

Here’s the thing: a lot of small business owners treat bookkeeping as an afterthought, something to deal with at tax time. But every financial statement you’ll ever look at, your balance sheet, your income statement, your cash flow statement, is built entirely on the foundation of accurate journal entries.

A few reasons they matter so much:

- They create an audit trail, showing exactly what happened and when

- They ensure your financial statements are accurate and reliable

- They help catch errors or fraud early, before they snowball

- They’re often required for tax compliance and reporting

Quick takeaway: Treat your entries as an ongoing habit, not a once-a-month scramble. Consistency prevents small mistakes from becoming big problems.

Types of Journal Entries You Should Know

Not every entry looks the same. Depending on the situation, you’ll typically encounter one of the following types.

Standard Entries

Used for everyday transactions, such as recording a sale or a purchase.

Adjusting Entries

Made at the end of an accounting period to account for things like accrued expenses, prepaid items, or depreciation.

Closing Entries

Used to reset temporary accounts (like revenue and expenses) at the end of a fiscal year.

Reversing Entries

Optional entries made at the start of a new period to cancel out certain adjusting entries from the previous one.

Quick takeaway: If you’re new to bookkeeping, start by mastering standard entries before moving on to adjusting and closing entries. Build the foundation first.

Step-by-Step: How to Record a Journal Entry Correctly

Let’s get practical. Here’s the process, step by step.

- Identify the transaction — What actually happened? A sale, an expense, a loan payment?

- Determine which accounts are affected — This could be cash, accounts receivable, inventory, and so on

- Decide which accounts are debited and which are credited — Remember, assets and expenses increase with debits; liabilities, equity, and revenue increase with credits

- Record the date and a clear description — Future you will thank present you for this

- Verify that debits equal credits — If they don’t, something’s off

- Post the entry to the general ledger — This moves the transaction into your permanent records

That said, this process becomes second nature with repetition. The first few entries might feel slow and confusing, but it clicks faster than you’d expect.

Quick takeaway: Double-check your debits and credits before posting. A five-second review now saves an hour of troubleshooting later.

Common Mistakes to Avoid

Even experienced bookkeepers slip up sometimes. Here are the mistakes that show up most often.

- Forgetting to balance debits and credits — the single most common error

- Misclassifying accounts, such as recording an expense as an asset

- Skipping documentation, leaving no clear description of what the transaction was for

- Not recording entries in real time, leading to a pileup of forgotten transactions

- Ignoring adjusting entries at the end of a period, which throws off financial statements

In practice, most of these mistakes come down to rushing. Slowing down, even slightly, tends to fix most of them.

Quick takeaway: Set a recurring reminder to record entries weekly rather than letting transactions pile up for month-end.

Journal Entry Examples for Common Transactions

Sometimes it helps to see it in action. Here are a few everyday examples.

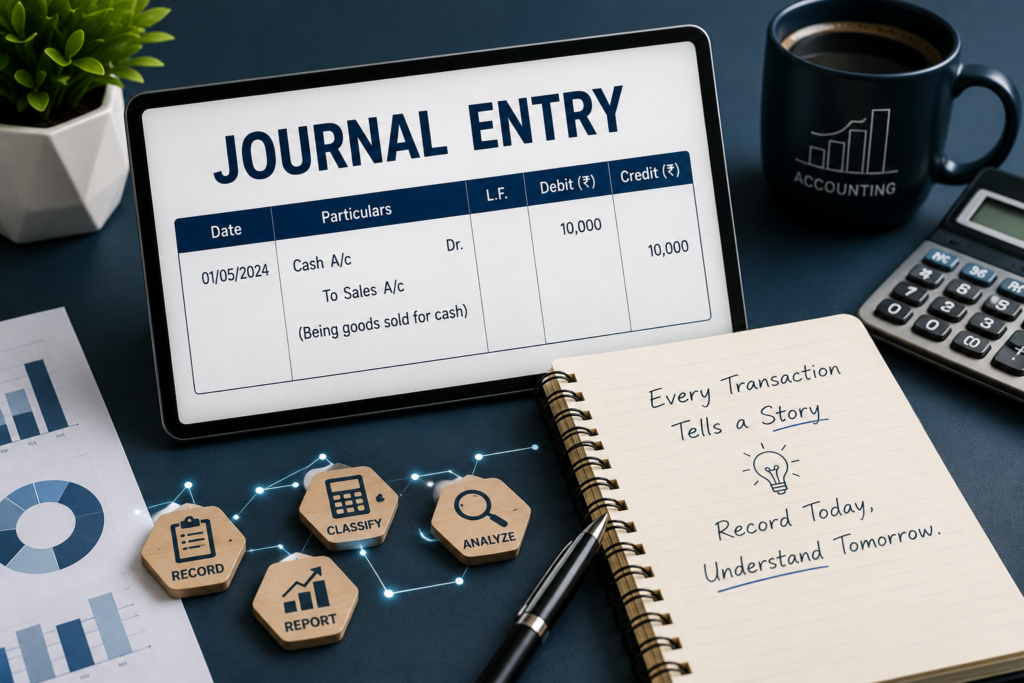

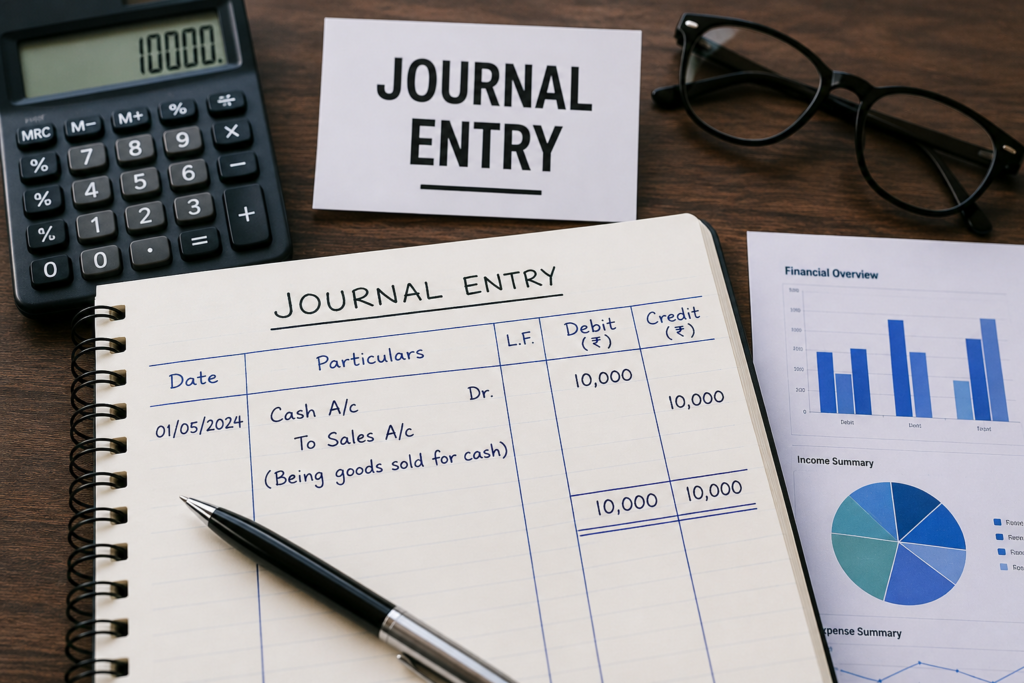

Example 1: Cash Sale Debit Cash, Credit Sales Revenue

Example 2: Purchasing Office Supplies on Credit Debit Office Supplies Expense, Credit Accounts Payable

Example 3: Paying Off a Loan Debit Loan Payable, Credit Cash

Example 4: Recording Depreciation (Adjusting Entry) Debit Depreciation Expense, Credit Accumulated Depreciation

Quick takeaway: Keep a running reference sheet of common entries specific to your business. It saves time and reduces second-guessing.

Tools That Make Journal Entries Easier

You don’t need to do all of this by hand anymore, though understanding the manual process is still valuable, especially for catching errors software might miss.

Popular tools that simplify the process include:

- QuickBooks, widely used by small to mid-sized businesses

- Xero, known for its clean interface and automation features

- NetSuite, better suited for larger or more complex organizations

- Excel or Google Sheets, still a reliable option for very small operations or learning purposes

Quick takeaway: Even with automated software, periodically review a sample of your entries manually. It keeps your understanding sharp and catches errors automation might overlook.

When to Bring in a Professional

Rhetorical question worth asking: at what point does DIY bookkeeping stop making sense? For many small business owners, that point comes when transaction volume increases, or when tax complexity grows.

Signs it might be time to hire a bookkeeper or accountant:

- You’re spending more time on books than on your actual business

- You’re unsure how to handle adjusting or closing entries

- Your business is growing and transactions are becoming more complex

- You’ve had errors that led to inaccurate financial statements

Quick takeaway: There’s no shame in outsourcing this. A good bookkeeper often pays for themselves through the errors and time they save you.

5. FAQs

Q1: What is a journal entry in accounting? A journal entry is a record of a financial transaction in a company’s accounting system, following the double-entry method. It always includes a debit and a matching credit that keep the books balanced.

Q2: Why must a journal entry always balance? Because accounting relies on the double-entry system, where every transaction affects at least two accounts. If debits don’t equal credits, it signals an error somewhere in the recording process.

Q3: What’s the difference between a journal entry and a ledger entry? A journal entry is the initial record of a transaction, while a ledger entry is where that transaction gets posted and organized by account. The journal comes first, the ledger organizes it afterward.

Q4: Can I create a journal entry without accounting software? Yes, journal entries can be recorded manually using a simple spreadsheet or physical ledger. Many small businesses start this way before moving to accounting software as they grow.

Q5: What are adjusting journal entries used for? Adjusting entries are made at the end of an accounting period to account for things like accrued expenses, prepaid costs, or depreciation, ensuring financial statements reflect accurate, up-to-date figures.

Q6: How often should I record journal entries? Ideally, journal entries should be recorded as transactions happen, or at least weekly. Waiting until month-end increases the risk of forgetting details or making classification errors.

Final Thoughts

A journal entry might seem like a small, routine task, but it’s genuinely the foundation of every accurate financial record your business will ever produce. Get comfortable with the basics, stay consistent, and don’t be afraid to double-check your work.

Whether you’re doing this manually or with the help of accounting software, the principles stay the same. Debits and credits, recorded accurately and consistently, are what keep your books, and your business decisions, on solid ground.

You can find detailed guidance on standard accounting principles through the Financial Accounting Standards Board (FASB), which sets the foundational rules most U.S. accounting practices follow.