Imagine a customer browsing your website or walking into your store. They find exactly what they want, but the price tag makes them hesitate. They walk away, and you lose a sale.

This happens thousands of times a day. But what if you could remove that price barrier instantly?

That is exactly where customer financing solutions come in. By allowing buyers to split their purchases into manageable payments, you empower them to buy what they need right now. In this comprehensive guide, we will break down everything you need to know about setting up flexible payment options, avoiding common pitfalls, and skyrocketing your revenue in 2026.

What Are Customer Financing Solutions?

Customer financing solutions (often called consumer financing or point-of-sale financing) are payment plans that allow consumers to purchase goods or services immediately while paying for them over time.

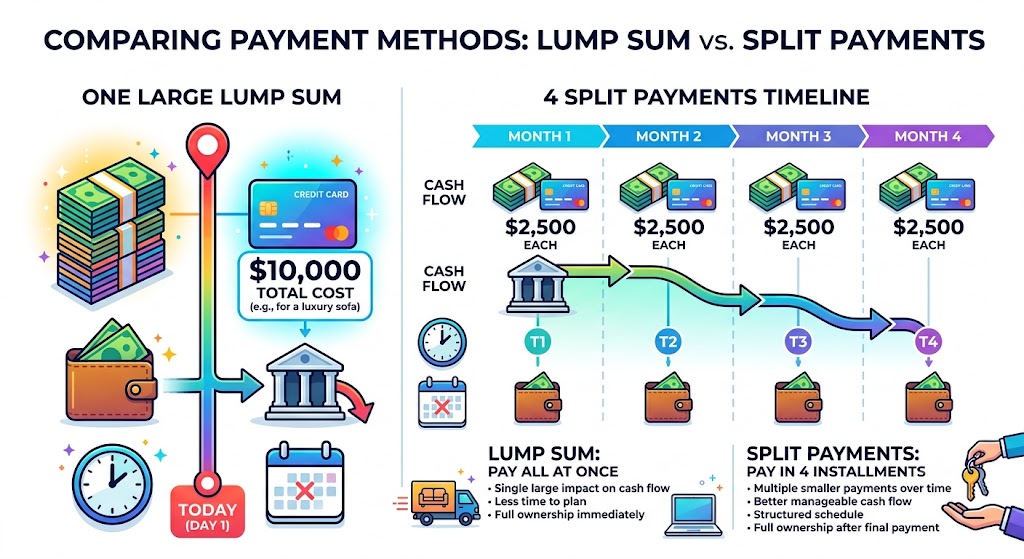

Instead of paying a large lump sum upfront, the customer pays in smaller, scheduled installments. Typically, a third-party financial provider handles the risk, pays you (the merchant) upfront, and collects the payments from the customer.

These solutions come in a few common formats:

- Buy Now, Pay Later (BNPL): Usually splits purchases into four interest-free payments.

- Installment Loans: Longer-term financing (6 to 36 months) is often used for high-ticket items like furniture, electronics, or home repairs.

- Store Credit Cards: Branded revolving credit lines for loyal, repeat shoppers.

Why Customer Financing is Important for Your Business

Adding flexible payment options to your checkout process is no longer just a “nice-to-have” feature; it is a critical growth engine. Here is why you need to pay attention:

1. Skyrocket Conversion Rates

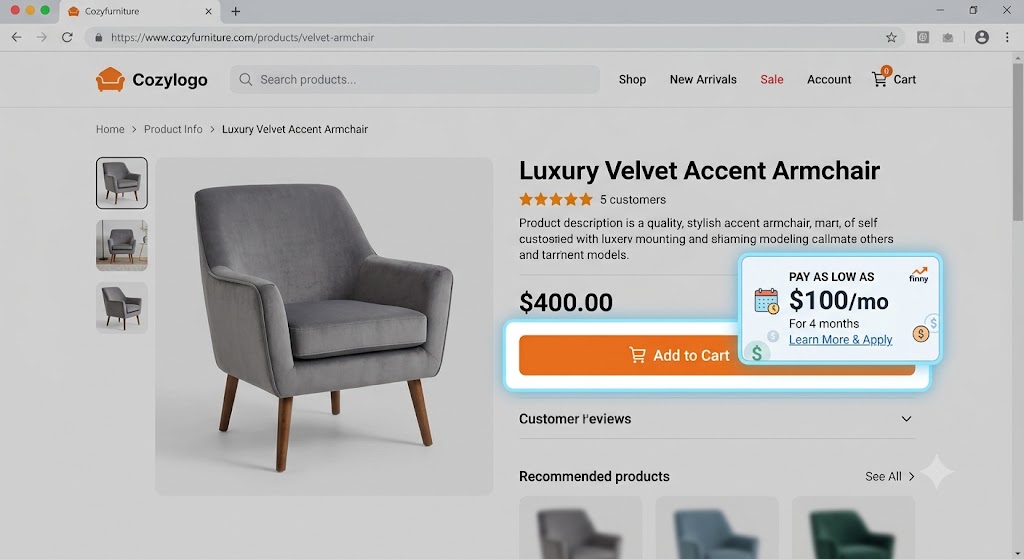

Price friction is the number one reason for cart abandonment. When a customer sees they can pay $50 a month instead of $600 today, the purchase feels much more attainable. Giving customers the option to finance directly at checkout turns browsers into buyers.

2. Boost Average Order Value (AOV)

When budget constraints are lifted, customers are far more likely to upgrade their purchases.

- Real-Life Example: A customer looking at a basic $800 mattress might upgrade to the $1,200 luxury model if the difference is only a few extra dollars per month on their payment plan. Many merchants report a 20% to 30% increase in AOV after introducing financing.

3. Build Unbeatable Customer Loyalty

Consumers return to businesses that make their lives easier. By providing smooth, transparent customer financing solutions, you build trust. If a customer knows they can affordably shop at your store, they will choose you over a competitor who demands full payment upfront.

Suggest External Link: Link to a high-DA study by Forbes or Shopify on how BNPL impacts consumer spending habits.

Step-by-Step Guide to Offering Customer Financing

Ready to integrate these solutions into your business? Follow this simple roadmap to get started.

Step 1: Analyze Your Customer Base

Before you choose a financing partner, you need to understand your audience.

- Are you selling $50 apparel or $5,000 home renovations?

- Do your customers prefer short-term, interest-free plans (BNPL) or do they need multi-year installment loans? Mapping your typical customer’s financial needs will dictate the type of software you choose.

Step 2: Choose the Right Financing Partner

Not all providers are created equal. You need a partner that offers good approval rates and fair terms.

| Feature | Buy Now, Pay Later (e.g., Klarna, Afterpay) | Traditional Installment (e.g., Affirm, Synchrony) |

| Best For | Low to medium ticket ($50 – $1,000) | High ticket items ($1,000 – $10,000+) |

| Interest | Usually 0% for the customer | Often carries an APR based on credit |

| Term Length | 6 weeks (Pay in 4) | 6 to 60 months |

Step 3: Integrate Point-of-Sale Tech

Whether you run a brick-and-mortar shop or an e-commerce store, the financing option must live inside your checkout process. Most modern providers offer simple plugins for platforms like Shopify, WooCommerce, and Magento. Ensure the integration is seamless—if it takes more than a few clicks to apply, customers will abandon the cart.

Step 4: Market Your Payment Options

Having financing is useless if nobody knows about it.

- Put banners on your homepage.

- Add dynamic pricing to product pages (e.g., “Or pay just $25/mo”).

- Mention flexible payments in your email marketing and social media ads.

Common Mistakes to Avoid with Consumer Financing

Even with the best intentions, businesses can mess up their financing rollout. Avoid these costly errors:

- Hiding the Fees: Always be transparent. If the customer has to pay interest, or if you are eating a large merchant fee, know the math beforehand. Never let customers get hit with “surprise” late fees without a clear warning.

- Complicating the Checkout: The application process should take seconds, not minutes. Avoid partners that require lengthy credit applications that take users away from your website.

- Only Offering It at the End: If a customer doesn’t know you offer financing until they reach the final checkout page, you’ve already lost the ones who bounced from the product page because of the price.

Pro Tips for Better Financing Results

Want to get the absolute most out of your customer financing solutions? Keep these expert strategies in mind:

- Train Your Sales Team: If you have physical stores or a phone sales team, ensure they know how to pitch financing. It should be presented as a helpful tool (“We have a great 0% interest plan for this”) rather than a last resort.

- Use Omnichannel Financing: Ensure the customer gets the exact same financing options whether they buy from you on Instagram, on your website, or in-store.

- Monitor Your Margins: Financing partners charge merchant fees (often 2% to 6% per transaction). Ensure your profit margins can absorb this cost, or adjust your pricing strategy accordingly. The increase in sales volume usually makes up for the fee, but you must track the math.

Frequently Asked Questions (FAQs)

Who takes the risk if a customer doesn’t pay?

The third-party financing provider takes the risk. You, the merchant, are paid upfront (minus the provider’s fee). If the customer defaults, the financing company handles the collections, not you.

Are customer financing solutions only for B2C?

No! B2B customer financing is growing rapidly. Many providers now offer net-30, net-60, or specialized invoice financing specifically for business-to-business transactions, helping companies manage cash flow.

Does applying for financing hurt a customer’s credit score?

In most cases, no. Modern BNPL and point-of-sale financing providers use a “soft pull” on the customer’s credit to check eligibility, which does not impact their credit score.

How much does offering financing cost the merchant?

Typically, financing companies charge a merchant discount rate per transaction. This can range anywhere from 2% to 8%, depending on the term length and the provider you choose.

Conclusion: Take Action Today

Integrating customer financing solutions is one of the fastest, most effective ways to remove buyer friction, increase your average order value, and build a base of loyal customers. By choosing the right partner, integrating the tech smoothly, and marketing the options clearly, you can set your business up for massive success in 2026 and beyond.

Don’t let another customer walk away because of upfront costs. Give them the flexibility they deserve, and watch your sales grow.

Ready to upgrade your checkout experience?

👇 Comment your thoughts below on how financing could help your business, share this article with your network, or subscribe for updates to get more expert business growth strategies delivered straight to your inbox!